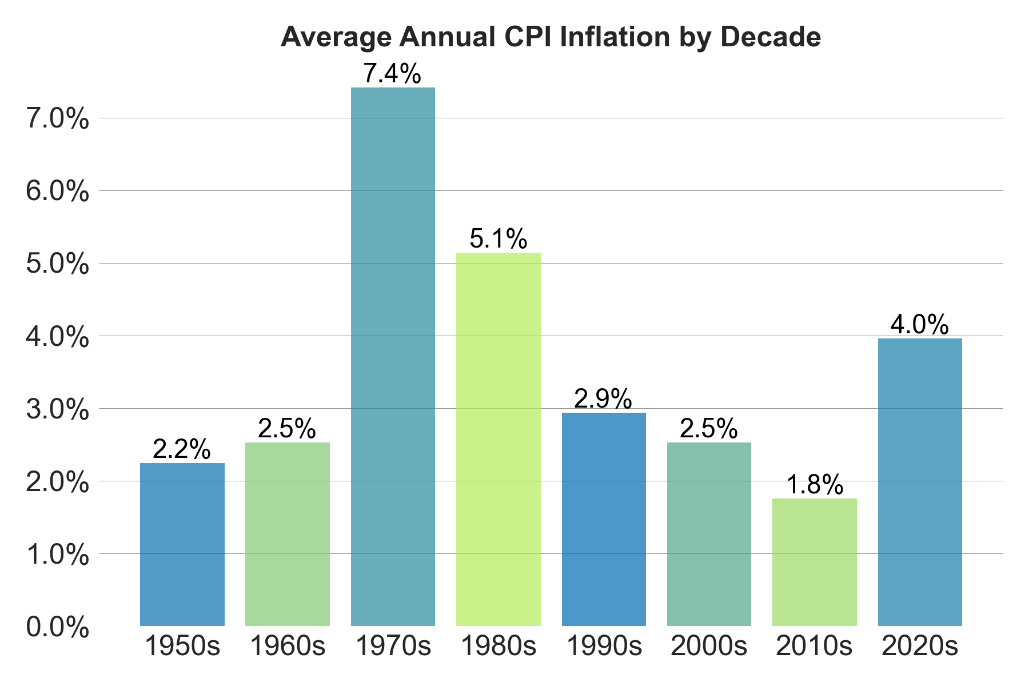

While landing in line with consensus, this week’s CPI reading in the U.S. reinforces long-term changes in inflation and rates regime. Narratives aside, these changes are significant and lasting enough to challenge the LP-GP allocation approach that evolved in a different era.

The fixed 8% preferred return in closed-end equity funds is commonly described as LP protection, but in substance it is a nominal allocation breakpoint between LP and GP economics. This number for all seasons became embedded in the early decades of the industry during decades of lower and more stable inflation, falling nominal interest rates, cheaper leverage, and multiple expansion.

Source: Bureau of Labor Statistics and Cadwalader, Wickersham & Taft LLP.

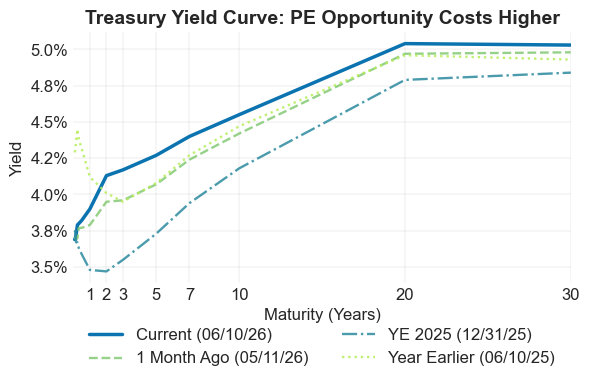

The 2020s are unfolding differently: Real risk-free rates are no longer negligible; Treasury supply and fiscal deficits put pressure on term premium; higher financing costs reduce debt capacity and exit multiples; slower realizations increase the opportunity cost of trapped capital; and inflation has eroded real returns.

For LPs, the impact is straightforward: Higher Treasury rates raise the opportunity cost of locking up capital while elevated inflation reduces the real value of a nominal 8% pref return. These basic mechanics are often overlooked in the fundraising discussion, but are relevant in explaining the 12.5% CAGR in global private funds AUM during the 2010s dropping to 4.6% in the 2020s based on Preqin data.

Source: U.S. Department of the Treasury and Cadwalader, Wickersham & Taft LLP.

In previous decades, an 8% pref rate meant LPs achieved a meaningful real return before GP carry kicked in. (The GP catch-up can sharply accelerate the transfer of economics after the pref is met.) Given a 4% average annual inflation in so far in the 2020s, that real return looks more modest. An updated version of real return alignment would potentially consider Treasury yields, inflation, an illiquidity spread, and a nominal floor. A more dynamic approach would consider whether LPs are adequately compensated for inflation, illiquidity and duration based on the macro environment ahead of GP participation.

For fund finance lenders, this is a qualitative point. While it doesn’t directly affect the borrowing base, a more LP-favorable waterfall would be a credit positive at the margin because it improves the economic position, alignment, and presumably the behavior of the LPs supporting that collateral. In the current inflation, rate, and DPI environment, that qualitative benefit is more relevant than it was when the standard pref rate offered a more meaningful real-return threshold.

Perhaps updating the configuration matters for fundraising as well. For GPs, the established waterfall structure is easy to administer and offers consistency in economics. But this consistency may come at the cost of imbalances manifesting in fundraising when market conditions make the LP proposition less compelling.